We’re pretty sure everyone reading this already knows about the changes HUD announced Tuesday, but if not you should definitely check them out.

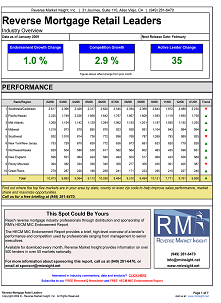

So once you pick yourself up off the floor, the good news is that HECM endorsements rose 15.8% in August to 4,927 loans. Small consolation, but at least the rear view mirror view is pretty good.

Here’s our take after a few days to think about it, with the caveat that we expect nobody has figured out yet exactly how to position for the industry’s new reality:

- The most significant change is the effective removal of principal limit factor floors. By creating higher PLF curves at interest rates going all the way down to 3%, HUD has created a strong competitive incentive to reduce/eliminate the excess margin that was creating gain on sale revenue and supporting high marketing costs. That probably means minimal loan sale premium and the return of origination fees.

- Next up is the reduction of PLF curves at each expected rate by ~20%. A 5% expected rate loan after October 2 gets a consumer 20% less available principal limit than before that date. So, a rush to get borrowers in before the deadline at the same time everyone figures out how to survive under the new rules.

- Lastly, an increase in upfront mortgage insurance premium for borrowers drawing less than 60% in the first 12 months from 0.5% to 2%. If the borrower of the future is the financial planning customer looking to leverage a HECM to mitigate sequence of returns risk then HECM just became substantially more costly as an option to do that.

We have more thoughts about what this might mean for the future of the industry, but for now we’ll leave you with a link to HECM Lenders for last month and a hope that you thoroughly enjoy the holiday weekend!

If your company is FHA approved check out the rankings on page 5 of the report below. If your company is not FHA approved, watch out for our next edition of HECM Originators to find your ranking!

Click the image below for the full report.